It is made of pure cotton Cloth, and some fabrics are chemically treated due to different needs Cotton Cloth Wheel,Cotton Buffing Wheel,Buffing Cloth Wheel,Cotton Polishing Wheel Jiangmen Gude Polishing Equipment Co., Ltd , https://www.kokipolishing.com

Abstract When LME copper stocks hit a 10-year high, manufacturing companies are still paying the highest spot pick-up premium in nearly seven years. This is due to financial transactions locking in large volumes of copper, while long queues outside warehouses persist. Although LME inventory has more than doubled over the past year and the first major copper oversupply since 2009 has occurred, the cost of extracting copper has increased, and waiting times have become longer. According to Bloomberg, Shanghai buyers are paying $135/ton more than LME futures prices—up from $55 last year. Some Malaysian manufacturers have even stopped buying from local LME warehouses because wait times for pickup have stretched from three days in early 2012 to three months today.

Although copper prices have dropped 29% from their two-year peak, manufacturers aren’t necessarily benefiting because financial agreements have restricted the availability of copper in the open market. Société Générale estimates that up to 30% of LME-registered copper is tied to such financial arrangements. Currently, 84% of LME copper is concentrated in just three locations, and delays caused by strikes at Chilean ports have further extended pickup wait times.

So far this year, the LME copper benchmark price has fallen 8.4% to $7,265.5/ton. Goldman Sachs has also lowered its 12-month copper price forecast to $7,000/ton. Meanwhile, Standard Chartered Bank predicts global copper output will rise 4.3% to 21.1 million tons this year, while demand is expected to grow 2.2% to 20.9 million tons. Despite this, the International Copper Research Group in Lisbon notes that copper has been in short supply for the past three years.

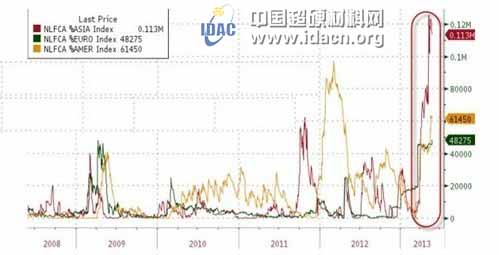

On the other hand, the number of pickup applications for LME copper has reached a record high recently. As shown in the chart below, demand from Asia—represented by the red line—is particularly strong:

According to ZeroHedge, although many media outlets see the surge in LME copper spot demand as a sign of “recovery,†the situation may not be so straightforward. The spike is largely driven by Asian demand, likely from China, which suggests deeper economic implications. While the exact reason remains unclear, the recent surge in pickup requests closely mirrors Goldman Sachs’ discussion about the end of the “unlimited copper financing†era.

China’s repeated mortgage financing activities have created a system where copper stored in bonded zone warehouses could fail to meet the collateral requirements when letters of credit mature. This might explain the sudden increase in LME copper pickup requests, reflecting urgent needs from Chinese trading companies to support ongoing financing deals.

As a reminder, a month ago, the sharp drop in gold prices coincided with a surge in physical gold demand. Similarly, the current jump in spot copper demand should be carefully monitored to understand the real market dynamics.

Looking back at the article “The End of the Copper Financing Era Is China’s Lehman Moment?†it highlights how copper financing transactions work. At each stage, a ton of copper in the Shanghai Bonded Zone can support a letter of credit liability worth tens of times its value. During the 6-month validity period of a letter of credit, these steps can be repeated up to 10–30 times, depending on document processing time. As a result, the total nominal value of a letter of credit based on a certain amount of bonded or imported copper can reach 10–30 times the actual physical copper value in a year.

Therefore, the rising demand for copper spot is driven by the need for real collateral behind the letters of credit. Similar to the reserve banking system, banks must meet withdrawal demands suddenly. This could explain why copper prices have risen sharply but remain weak overall. If the copper used as collateral is returned to the issuing bank, the financing transaction would end, and the bank would no longer hold such high-value goods. In that case, the market could return to an oversupply situation.